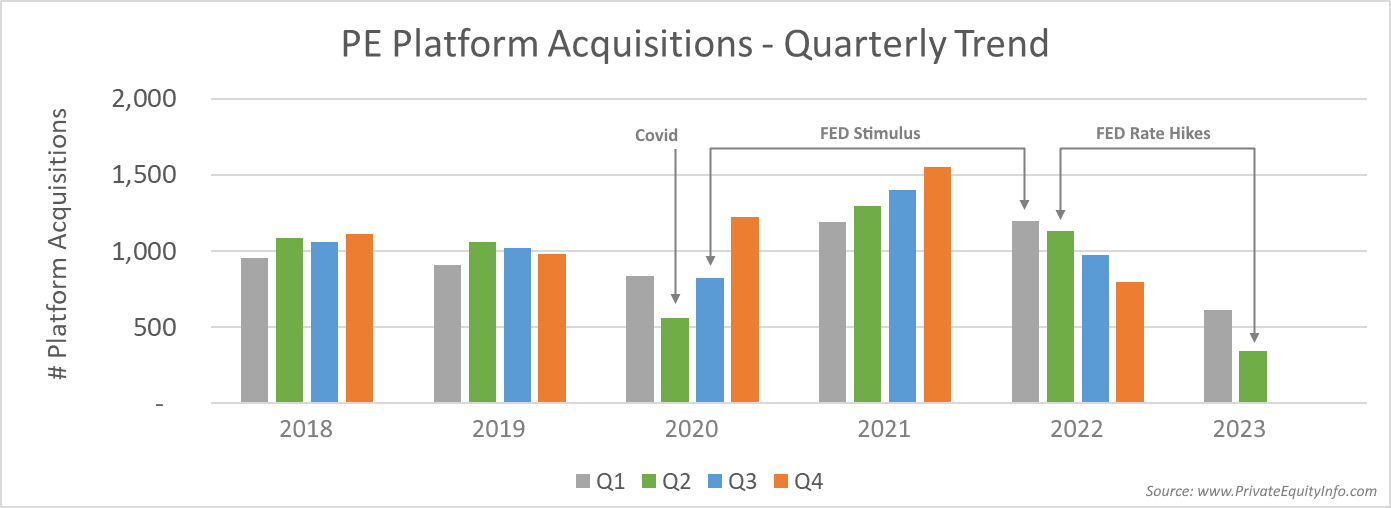

The number of private equity platform acquisitions and add-on acquisitions dropped significantly in 2023, showing the broad industry impact of recent Federal Reserve rate increases and other macroeconomic trends.

According to new data from Private Equity Info, platform acquisitions this year have dropped considerably, even below the dip caused by the uncertainty of COVID-19 in the second quarter of 2020, and precipitously from the peak in 2021.

Private Equity Info analyzed 322 platform acquisitions and 408 add-on investments that were completed in the second quarter. The company tracks private equity acquisitions among 34 million continuously updated data points in the M&A industry.

Private equity platform investments are highly correlated with broader macroeconomic factors, particularly federal actions. This is the real-world impact of government stimulus and contractions, played out across the private equity and M&A industry at large.

This variability in platform acquisitions not only impacts the velocity of M&A transactions, but also valuations, as supply and demand imbalances occur during deal peaks and troughs. The back half of 2021 and the first half of 2022 were seller’s markets, with inflated valuations driven by excess capital and low interest rates on debt.

Are we now moving to a buyer’s market or did the recent peak in Platform acquisitions only clear a bulge in the deal pipeline?

One signal is found in PEI's data on the pace of add-on investments. An increase in the number of add-on acquisitions would signal a focus on lower risk, easier-to-finance investments that would complement the peak of platform acquisitions in 2021 and the first half of 2022.

But private equity is acquiring fewer add-on investments, as well, as depicted in the chart below. This is not an industry shift from platforms to add-on investments, it is a shift in private equity's overall appetite for acquisitions.

If you'd like to explore the data, Private Equity Info is offering a free downloadable list that includes the 300+ platform acquisitions completed in the second quarter, as well as more complete lists of platform and add-on acquisitions that include more detailed fields such as executive contact information, available for purchase in the PEI Shop.